.svg)

NBFC Education Loan in India

Looking to fund your higher education but facing hurdles with traditional banks? That's where NBFC (Non-Banking Financial Company) education loans in India are emerging as a strong alternative. They offer quicker approvals, flexible criteria, and funding even when banks say no. Especially helpful for students with no collateral or low co-applicant income.

In this blog, we’ll explore all about NBFCs. What they are, how they work, their features, interest rates, eligibility, and the types of courses they cover, thus helping you make an informed choice for your academic journey.

By the end of this blog, you will know

- NBFCs offer a strong, hassle-free alternative to traditional banks for education loans in India. RBI-regulated, they provide quicker approvals and flexible criteria for students without collateral or low co-applicant income.

- They make education loans accessible through collateral-free options, evaluating academic performance and earning potential over assets.

- NBFC education loans cover a wide array of courses - from traditional degrees to international programs - with 100% financing for all expenses.

- Eligibility requires Indian citizenship (18-35 years), good academics, and university admission. NBFCs offer significantly faster processing with minimal documentation and flexible repayment including moratorium periods.

What are NBFCs?

NBFCs, or Non-Banking Financial Companies, are financial institutions that offer services similar to banks—but without holding a full banking license. They are regulated by the Reserve Bank of India (RBI) and can provide loans, credit facilities, insurance, and investment options. However, unlike banks, NBFCs cannot accept demand deposits such as savings or current accounts.

For students, NBFCs have emerged as a vital source of education financing. They often provide more flexible terms, faster processing, and wider course coverage compared to traditional banks, making higher education loans more accessible. New-age NBFCs and Fintechs such as Propelld, that disburses education loans through its RBI-registered NBFC, are known for their student-centric approach, offering customized repayment options and quicker approvals, which especially benefits those pursuing non-traditional or specialized courses.

NBFC Market Impact & Growth

India's NBFC sector has experienced remarkable expansion, becoming a cornerstone of the country's financial ecosystem:

Market Size & Reach:

- 9,000+ registered NBFCs currently operating in India

- 3rd largest non-banking financial sector globally

- Education loans among fastest-growing NBFC segments (CRISIL report)

Economic Contribution:

- GDP contribution growth: From 18% (2002) to 60% (2020)

- Credit gap bridging: Serving underbanked segments effectively

Sector focus: Education, healthcare, rural development financing

NBFC Education Loan Interest Rates

Comparing NBFC education loan interest rates is absolutely essential for making an informed decision. Unlike banks, NBFCs often provide quicker approvals, flexible collateral requirements, and customized repayment options.

Below is a comparison of the top NBFCs for education loans in India, including loan amounts, processing fees, and repayment tenure.

|

NBFC |

Maximum Loan Amount |

Interest Rate (p.a.) |

|

Up to ₹60 Lakhs |

16.5% – 19.5% |

|

|

Up to ₹80 Lakhs |

9.95% – 13.25% |

|

|

Up to ₹50 Lakhs |

9.5% – 14% |

|

|

Up to ₹65 Lakhs |

11% – 13.5% |

|

|

Up to ₹15 Lakhs |

15% – 45% |

|

|

Up to ₹40 Lakhs |

12% – 14% |

|

|

Up to ₹50 Lakhs |

11.5% – 15% |

|

|

Up to ₹30 Lakhs |

13% – 20% |

|

|

Up to ₹25 Lakhs |

11% – 14% |

|

|

Up to ₹30 Lakhs |

12% – 14% |

*Propelld in itself is not an NBFC but disburses loans through its RBI-registered NBFC, which means we follow strict compliance, fair lending practices.

Why Rates Vary?

Rates depend on factors like academic performance, co-applicant income, and target university (see engineering BTech loan rates). For example, students with strong entrance exam scores, high ranks, good academic background or admissions to top-ranked institutions may qualify for the lower end of the band.

Before finalizing, always check whether the NBFC has tie-ups with your university. This can impact both approval speed and loan terms.

Top NBFCs for Education Loans in India: Detailed Analysis 2026

Several leading NBFCs in India offer student-friendly education loans with flexible repayment, quick approvals, and higher loan limits than traditional banks. Below is a detailed analysis of the top NBFCs for education loans in 2026:

Propelld focuses on accessible education financing with flexible eligibility criteria and transparent processes.

Key Highlights:

- ✓ Flexible terms with relatives allowed as co-applicants

- ✓ Hassle-free, collateral-free loans with minimal documentation

- ✓ 100% expense coverage based on a student's academic potential & future college

Loan Details:

- Loan Amount: Up to ₹40 lakhs*

- Interest Rate: 12% - 14% p.a.

- Processing Fee: 1% - 2%

- Repayment Tenure: Up to 10 years

- Eligibility: Indian residents, age 18+

*Loan amounts up to ₹40L for domestic courses, with higher ticket sizes considered for abroad studies based on profile and university.

Best For: Students needing flexible eligibility criteria, no collateral loan with comprehensive expense coverage.

Credila stands out with the highest loan limits and competitive rates, making it ideal for premium courses and international studies.

Key Highlights:

- ✓ Highest loan amount – Up to ₹80 lakhs

- ✓ Competitive rates starting from 9.95%

- ✓ Established reputation with extensive institution network

Loan Details:

- Loan Amount: Up to ₹80 lakhs

- Interest Rate: 9.95% - 13.25% p.a.

- Processing Fee: 1% of loan amount

- Repayment Tenure: Up to 12 years

- Moratorium: Simple/Partial interest during course

Best For: Students targeting premium institutions requiring substantial funding.

Auxilo offers the most competitive starting rates among NBFCs, making it attractive for cost-conscious borrowers.

Key Highlights:

- ✓ Industry-low rates starting from 9.5%

- ✓ Flexible processing fees from 0.5%

- ✓ Extended tenure options up to 12 years

Loan Details:

- Loan Amount: Up to ₹50 lakhs

- Interest Rate: 9.5% - 14% p.a.

- Processing Fee: 0.5% - 2%

- Repayment Tenure: 10-12 years

- Eligibility: Full-time course enrollment

Best For: Students seeking lowest possible interest rates with flexible terms.

InCred combines competitive rates with a digital-first approach, offering one of the fastest approval processes in the NBFC sector.

Key Highlights:

- ✓ Quick approvals through tech-enabled processing

- ✓ Substantial limits up to ₹65 lakhs

- ✓ Flexible repayment during and after studies

Loan Details:

- Loan Amount: ₹40 lakhs – ₹65 lakhs

- Interest Rate: 11% – 13.5% p.a.

- Processing Fee: 0.5% – 2%

- Repayment Tenure: 10–12 years

- Eligibility: Admission in reputed institutions

Best For: Students pursuing short-term courses or skill development programs with immediate funding needs

Established Player with Extended Tenure

Avanse provides substantial loan amounts with longer repayment periods, though at higher interest rates compared to newer market entrants.

Key Highlights:

- ✓ High loan limits up to ₹60 lakhs

- ✓ Extended tenure up to 12 years

- ✓ Comprehensive coverage for all education expenses

Loan Details:

- Loan Amount: Up to ₹60 lakhs

- Interest Rate: 16.5% – 19.5% p.a.

- Processing Fee: 1% – 2%

- Repayment Tenure: Up to 12 years

- Eligibility: Indian residents, age 18+

Best For: Students needing substantial funding with longer repayment periods, willing to pay premium rates for established service.

*Propelld in itself is not an NBFC but disburses loans through its RBI-registered NBFC, which means we follow strict compliance, fair lending practices.

Get you Education Loan Approved in Just 2 Days

Key Features of NBFC Education Loans

Non-Banking Financial Companies (NBFCs) have become a popular choice for students looking for faster and more flexible education loan options. Compared to traditional banks, NBFCs are known for quicker approvals, minimal documentation, and tailored repayment structures.

Let’s see the key features of NBFC education loans:

- Tuition and examination fees

- Hostel or accommodation charges

- Books, laptops, equipment, and study material

- Travel expenses (for study abroad loans)

- Insurance coverage for students or co-borrowers

- Tie-ups with universities for faster processing

- Customized repayment plans linked to employability

What is the Moratorium Period for NBFC Education Loans?

Most NBFCs offer a moratorium of 6–12 months post-course completion. Students usually pay simple/partial interest during studies, with full EMI starting after the grace period.

How NBFCs Transform Education Financing?

We have read the features of NBFC above. Now let’s see how these features help bridge the education financing gap for the segments that are not so easily covered by banks.

Addressing Traditional Banking Gaps: NBFCs fill critical credit voids left by conventional banks, particularly in:

- Alternative income assessment for self-employed families

- Lower credit score acceptance for first-time borrowers

- Faster disbursement for urgent admission requirements

- Flexible repayment options aligned with career timelines

- Student-Centric Approach: Unlike banks with standardized products, NBFCs often customize education loans based on:

- Course-specific requirements and earning potential

- Institution ranking and placement records

- Individual family financial situations

- Future income projections for repayment planning

Ready for hassle-free education financing? Propelld offers all above benefits with quick digital approvals.

NBFC Education Loan without Collateral

Education loans help students cover tuition, housing, books, and other academic expenses. NBFCs often provide such loans without requiring collateral, making them accessible to students without substantial assets.

These loans are granted based on creditworthiness, academic performance, and future earning potential. Applicants must meet specific eligibility criteria, including course duration and, in some cases, a co-borrower with a stable financial background.

Here are some top NBFCs offering education loans without collateral:

|

NBFC |

Maximum Loan Amount |

Interest Rate Range |

|

Avanse Education Loans |

Up to ₹60 lakh |

12.5% - 13.5% per annum |

|

Up to ₹80 lakh |

11.5% - 13.5% per annum |

|

|

Up to ₹50 lakh |

12.5% - 13.5% per annum |

|

|

Up to ₹40 lakh |

11% - 14% per annum |

|

|

InCred Education Loans |

Up to ₹65 lakh |

12.5% - 13.5% per annum |

To know more, explore collateral free education loans - check list of banks, eligibility, documents required, how to choose the right loan and get your application approved.

NBFC Education Loan Eligibility

While specific conditions may vary slightly between NBFCs, some general eligibility criteria for benefiting from an education loan from an NBFC include:

Generally between 18 and 35 years old.

Must be an Indian citizen.

A good academic record in previous studies. Completion of relevant pre-requisite courses may be required.

An acceptance letter from a recognized university/council for the chosen course. Must include registration and course legitimacy.

A co-signatory with a stable income is often required. Provides additional security to the lender.

Proof of financial capability to cover tuition and living expenses. Bank statements or income proof may be required.

Evidence of proficiency in the English language (e.g., IELTS, TOEFL) may be required for non-English medium students.

Some programs may require scores from specific entrance exams (e.g., GRE, GMAT) relevant to the field of study.

A personal statement or essay detailing motivation, goals, and reasons for pursuing the course.

Letters of recommendation from academic or professional references may be necessary.

Also, check out the eligibility for education loans.

Documents Required for NBFC Education Loan

Applying for an NBFC education loan requires both the student (applicant) and the co-applicant to submit specific documents. The co-applicant may be either salaried or self-employed, and the paperwork varies accordingly.

Let’s see the list of documents required by each person:

- Duly filled and signed loan application form

- KYC documents (PAN, Aadhaar, Passport, Voter ID, Driving License, or government-issued ID)

- Past academic records – all previous mark sheets and certificates

- Entrance exam results (if applicable to the course)

- Admission proof – admission/offer letter from the institute

- Passport size photographs

- Statement of expenses for the chosen course

- KYC documents (same as applicant)

- Latest 6 months’ bank account statement

- Existing loan statement (if applicable – last 1 year)

- Income documents:

- Last 3 months’ salary slips

- Form 16 for last 2 years

- Statement of assets and liabilities

- KYC documents (same as applicant)

- Latest 6 months’ bank account statement

- Existing loan statement (if applicable – last 1 year)

- Income documents:

- Business address proof

- Last 2 years’ IT returns

- TDS certificate (if applicable)

- Certificate of qualification (for professionals like doctors/CA)

- Statement of assets and liabilities

Types of Courses Covered by NBFC Education Loans

Here are the different types of courses covered by NBFC education loans, ensuring financial assistance for students pursuing diverse academic and professional paths.

Below are the traditional degree programs for which NBFCs provide education loans, ensuring students can pursue higher education without financial constraints.

| Type of Course | Description |

|---|---|

| Undergraduate Programs | Covers bachelor's degrees that typically last for four years. NBFCs usually provide loans for these programs. Offered by recognized universities and colleges in India. |

| Postgraduate Programs | Advanced programs that offer Master's degrees. Allow students to specialize in specific fields. NBFCs often support programs in diverse disciplines. |

Here are some professional courses that NBFCs support through education loans, helping students gain specialized knowledge and career growth.

| Type of Course | Description |

|---|---|

| Management Courses | Prepare individuals for managerial roles in organizations. Include MBAs and operations. NBFCs offer loans for management education to meet the demand for skilled professionals. |

| Law Courses | Train students to become lawyers or pursue legal careers. NBFCs typically finance LLB degrees and certificate courses in specific legal areas. |

| Medical Courses | Offer degrees like MBBS and postgraduate medical degrees. NBFCs may support various medical courses, depending on their internal policies. |

| Engineering Courses | Focus on the technical knowledge needed for different engineering disciplines. NBFCs often provide loans for BE/B.Tech degrees and postgraduate engineering programs. |

In addition to traditional and professional degrees, NBFCs also provide financial support for skill-based education and vocational training.

| Type of Course | Description |

|---|---|

| Vocational Courses | Substitute short-term programs that provide job-oriented skills. NBFCs recognize the importance of vocational education and offer loans for such courses. |

| Certificate Courses | Offer specialized skills in specific areas within a field. NBFCs may finance certificate courses that complement traditional degrees, catering to specific skill development needs. |

For students aspiring to study overseas, NBFCs offer loans to cover tuition fees, living expenses, and other costs associated with international education.

| Type of Course | Description |

|---|---|

| International Undergraduate Programs | Allow students to obtain degrees from universities outside India. NBFCs offer loans for study abroad programs. They consider factors like the university's reputation and the overall cost of living in the destination country. |

| International Postgraduate Programs | Enable students to pursue Master's degrees from universities abroad. Similar loan considerations apply, including university reputation and living costs. |

Let’s see some specific courses covered by NBFCs:

Getting an education loan for MBBS can really help ease the financial strain of medical school. It covers tuition and living expenses, letting future doctors focus on their studies without worrying about money.

BTech students can find relief with education loans that help pay for their engineering degrees. These loans cover tuition, books, and other costs, making it easier for them to chase their dreams in technology.

An education loan for an MBA can lighten the financial load of business school. It helps with tuition and living costs, so students can concentrate on developing their skills and making valuable connections.

Education loans for working professionals make it possible to learn new skills while still juggling a job. With flexible repayment options, these loans help individuals grow in their careers without added stress.

Nursing students can benefit from education loans that support the costs of their training. These loans cover tuition and supplies, helping passionate individuals pursue a fulfilling career in healthcare.

Education loans for pilot training can be a lifesaver for aspiring pilots. They help cover the expenses of flight school and necessary certifications, making it easier for them to achieve their dream of flying.

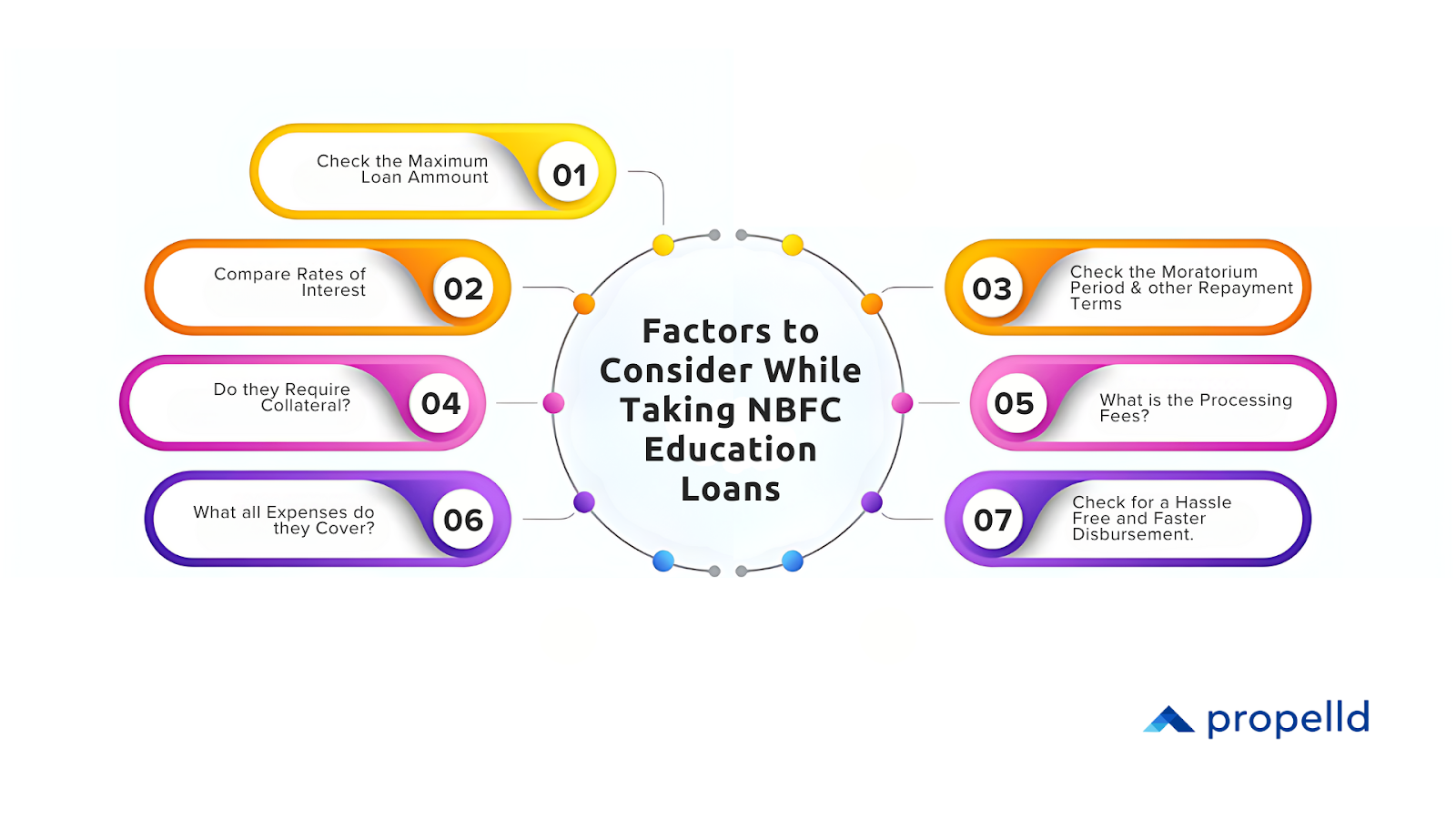

Factors to Consider While Taking NBFC Education Loans

NBFCs usually offer flexible repayment terms compared to traditional banks. Here are key aspects to consider:

The maximum amount of capital from NBFCs for education loans can vary a lot. It depends on which NBFC you go to, what course you want to study, and your personal details. But usually, you can borrow anywhere from Rs. 4 lakhs to Rs. 40 lakhs. Sometimes, NBFCs may even offer higher amounts for specific cases.

The interest rates on education loans from NBFCs are usually higher. This is because NBFCs cover students who might not have a long credit history. The interest rates can be between 10% to 17% per year. These rates can change depending on things like your credit scores, the course you're studying, and how much money you're borrowing.

Reimbursing the education loan usually takes around 5 to 10 years. Some NBFCs might give you a break from paying back the loan while you're still studying. This is called a moratorium period.

A key benefit of NBFC education loans is the freedom to repay early without extra charges. Unlike some banks that levy foreclosure penalties, most NBFCs including Propelld allow part-prepayments or full repayment without hidden fees. This flexibility helps students reduce their interest burden if they secure a job, receive scholarships, or wish to close the loan sooner, ensuring better financial control.

It might be a good idea to read the Education Loan Repayment Rules in India.

When applying for education loans, many borrowers worry about collateral requirements. However, with many NBFCs, including Propelld, you can access collateral-free education loans. This means you won’t need to pledge any assets, making it easier for students to secure funding without risking their valuable property.

Processing fees are an important aspect of education loans to consider. While some NBFCs may impose various fees, Propelld ensures transparency. We provide clear information regarding processing fees, so you understand all costs involved upfront without any hidden charges, making your loan experience straightforward and hassle-free.

The speed of loan processing can be crucial for students eager to begin their studies. Propelld boasts a processing time that is 10 times faster than traditional banks. This quick turnaround allows you to secure your education loan swiftly and start your academic journey without unnecessary delays.

When it comes to financing your education, it's vital to consider what expenses your loan covers. Propelld offers comprehensive coverage for all educational expenses, including tuition fees, accommodation, books, and living costs. This ensures that you have the financial support necessary to focus on your studies without worrying about unexpected expenses.

While some lenders may bundle insurance or other add-ons with education loans, most NBFCs, including Propelld, keep this optional. Students are clearly informed about any additional products and can decide based on their needs.

Is it Safe to Take an Education Loan from NBFC?

Yes, taking an education loan from an NBFC is absolutely safe. NBFCs are regulated by the Reserve Bank of India (RBI), which ensures compliance and borrower protection.

NBFCs are known for their USPs of quick fund disbursal, flexible repayment and personalised solutions. However, carefully reviewing the terms is indispensable.

Precautions to Keep in Mind

While NBFC loans are safe, it’s important to:

- Compare lenders – Interest rates, processing fees, and repayment flexibility can vary significantly.

- Read the fine print – Check for hidden charges, foreclosure penalties, or mandatory insurance.

- Assess repayment capacity – Ensure that the EMI schedule aligns with your future earning potential to avoid financial stress.

- Choose RBI-registered NBFCs – always verify that the lender is an authorized financial institution.

Get Education Loan for Any College in India. Propelld- An RBI Registered NBFC

Why are NBFCs a Better Option for an Education Loan? Bank vs NBFC

Unlike traditional banks, NBFCs offer more flexibility, faster processing, and better coverage for students pursuing diverse courses. Here’s a detailed comparison:

| Aspect | Banks (Public/Private Sector) | Non-Banking Finance Companies (NBFCs) |

|---|---|---|

| Course Flexibility | Banks cover graduate, post-graduate, diploma courses mainly in non-vocational streams. Some offer vocational courses case-by-case. | NBFCs cover a wider selection of courses, including offbeat and vocational courses globally. |

| Loan Coverage | Covers tuition fees, travel expenses, lab fees, exam fees, lodging fees, books, equipment, library fees, and related costs. | Covers 100% of tuition fees, travel expenses, lab fees, exam fees, lodging fees, books, equipment, library fees, and related costs. |

| Loan Procurement | More stringent rules, often requiring courses with job prospects. | Simpler terms, easier to procure for offbeat or unconventional courses. |

| Processing Time | Faster in private banks; public sector banks quicker based on customer relationships. | Generally faster, regardless of course type. |

| Processing Fees | Ranges from 0.5% to 2%. | Ranges from 1% to 2%. |

| Government Subsidy | Offers interest rate subsidy for weaker sections during the moratorium period. | No government subsidies available. |

| Security Collateral | Requires collateral for higher loan amounts: no security for loans below ₹4 lakhs, third-party guarantee for ₹4-7.5 lakhs, tangible collateral for above ₹7.5 lakhs. | Requires security based on loan amount and credit history. |

| Loan Amount | Upper limit between ₹20 lakhs and ₹30 lakhs based on course and university. | No cap on loan amount; structures loans based on student's needs and course type. |

| Charges | Includes processing, documentation, bounce, swap, prepayment, and late penalty charges. | Includes processing, documentation, bounce, swap, prepayment, and late penalty charges. |

| Interest Rates | Typically ranges from 10% to 17%, based on the base rate of the bank. | Offered as floating interest rates, generally in the same range as banks. |

| Moratorium Period | Ranges from 6 months to 1 year. | Generally 6 months. |

| Repayments | Can be repaid within 7 years, with interest repayments starting during the moratorium period. Principal repayments begin after securing a job. | Similar to banks; repayment within 7 years, interest during the moratorium, and principal afterward. |

| Documents Required | Admission Letter, Loan Application Form, Passport Photos, Study Cost Statement, PAN Card, Aadhaar Card, ID & Residence Proofs, Bank Statement, IT Returns, Liabilities & Assets Statement, Proof of Income. | Admission Letter, Loan Application Form, Passport Photos, Study Cost Statement, PAN Card, Aadhaar Card, ID & Residence Proofs, Bank Statement, IT Returns, Liabilities & Assets Statement, Proof of Income. |

| Customised Services | Some banks offer customized packages and doorstep services; pre-visa/pre-admission loan sanctions available. | Special services like pre-visa/pre-admission sanctions, fast-track loans, GRE score-based loans, and certificate of availability of funds. |

| Pre-closure Charges | Most banks do not levy pre-closure charges per RBI norms. | Pre-closure charges might apply, depending on closure reason, tenure, and borrower profile. |

| Concessions for Women | Often offer concessions on interest rates for women borrowers. | May not offer specific concessions for women. |

Education Loan Denied by Banks? NBFCs Can Still Fund it.

NBFCs have relaxed rules and easier processes when it comes to loan approvals. If you’ve faced roadblocks with traditional banks, you're not alone. Many students on platforms like Reddit have shared their struggles, often due to factors beyond their control.

Let’s look at two real cases that highlight how NBFCs can help where banks fall short:

Reddit User in r/Indians_StudyAbroad shared:

“I'm graduating with a Bachelor's in IT and got into ASU with a 307 GRE and 8-band IELTS. But HDFC rejected my loan due to my father’s low credit score. Despite my profile, they won’t fund me. I feel stuck—should I try other banks or will it be the same?”

Insight: Traditional banks heavily factor in your co-applicant’s credit history. NBFCs however, offer more flexibility, even allowing you to choose relatives other than your parents as co-applicants.

Another Reddit User on r/india posted:

“One of my friend (23yo) got into a top German university for master’s. She needs a loan of ₹10–12 lakhs, but does not have any collateral to pledge and her father, who’s retired with a small pension, doesn’t qualify as co-applicant. No bank or loan scheme is helping. Are there really no options for students from weak financial backgrounds?”

Insight: NBFCs are way quicker and less bureaucratic than banks. Even in cases where no collateral is available and there are issues with the co applicant, NBFCs can sanction the loan with an alternate co-applicant.

What do we infer from the above cases?

NBFCs can be your solution for education loan due to their:

- Flexible co-applicant criteria

- Lower dependency on CIBIL scores

- No Collateral Requirements even for higher loan amounts

- Faster processing timelines

Tip: If your parent isn’t eligible as a co-applicant, consider using a relative or sibling. Many NBFCs now allow this. About Collateral, most of them don't even ask for it!

Other Situations where NBFCs can be a Perfect Option for an Education Loan

Unlike some banks that ask you to pay part of the total cost yourself (called margin money), NBFCs often cover the entire amount, including tuition fees, living expenses, travel and exam charges. This helps students who can’t manage upfront payments.

NBFCs are more flexible. If you don’t have property or assets or your co-applicant (like a parent) has a weak credit score, NBFCs may still approve your loan based on your course, university, and future job potential.

NBFCs are usually more open to funding niche or less popular courses or admissions to a university that may not be on the bank’s approved list, whereas banks usually prefer traditional fields or well -known institutions.

NBFCs process loans faster than most banks. Many students say their NBFC loans were cleared in 7–15 days, while banks took longer.

Even if your or your co-applicant’s credit score isn’t great, NBFCs might still approve your loan. Many students online have shared stories of getting NBFC loans after being rejected by banks.

What is Margin Money in Education Loan?

Margin money is the portion of educational expenses a borrower must pay from their own funds, with the rest covered by the loan. Typically ranging from 5% to 15%, it reflects the borrower's financial commitment and varies based on whether the education is pursued in India or abroad.

Margin Money in NBFCs

NBFCs often provide more flexible loans compared to banks. Many of them, like Propelld, do not even require margin money. They offer to cover 100% of the education expenses, making them appealing for students seeking full financial support.

List of Banks Providing Education Loans in India

| Axis Bank | Federal Bank | Punjab & Sind Bank | State Bank of Hyderabad |

| Bank of Baroda | HDFC Bank | Punjab National Bank | State Bank of India |

| Bank of India | Indian Bank | Saraswat Bank | State Bank of Patiala |

| Bank of Maharashtra | Indian Overseas Bank | State Bank of Travancore | - |

| Canara Bank | IDBI Bank | Tamilnad Mercantile Bank | UCO Bank |

| Central Bank of India | Jammu And Kashmir Bank | Union Bank of India | - |

| City Union Bank | Karnataka Bank | - | Karur Vysya Bank |

| - | - | - | - |

Learn about the education loan moratorium period, a time when payments are temporarily paused. Find out how it can help manage finances and what you need to know during this period.

List of Non-Banking Finance Companies Providing Education Loans in India

|

Shriram Finance |

Saraloan |

LoanTap |

|

|

Eduvanz Education Loan |

Muthoot Finance |

Oxyzo Financial Services |

Navi |

|

Avanse Education Loan |

Mahindra Finance |

Recapita Finance |

Axio |

|

Lendingkart |

Ziploan |

TapStart |

|

|

U Gro Capital |

Home Credit |

Liquid Loans |

|

|

InCred Education Loans |

NeoGrowth |

PayU |

RupeeCircle |

|

Flexi Loans |

WeRize |

LenDenClub |

If you are considering an educational loan, check out Propelld.

Propelld understands the difficulties students encounter in funding their education. We offer superfast approvals, no collateral, minimal documentation, easy repayment plans, among many other USPs that fit each student's needs.