.svg)

Education Loans for MBBS Students

Pursuing an MBBS degree can be expensive, but education loans help ease the financial burden. These loans cover key expenses like tuition, accommodation, books, and more—making medical education more accessible for students from all backgrounds.

Key Takeaways

- Education loans for MBBS in India and abroad cover tuition, hostel, and other essential costs with both secured and unsecured options available.

- Secured loans for MBBS abroad can go up to ₹1.5–2 crore, while non-collateral options are available up to ₹75 lakh.

- Interest rates for MBBS education loans typically start at 8.55% for secured and 9.55% for unsecured loans.

- Students can use the Education Loan EMI Calculator to plan repayments effectively and manage EMIs after course completion.

- Understanding eligibility, process, and terms ensures smoother approval and affordable repayment planning.

Education Loans for MBBS India and Abroad

Education loans for MBBS, whether in India or abroad, cover a wide range of academic and living expenses, offer flexible repayment, and require co-applicants. Key differences lie in loan limits and collateral requirements.

|

Loan Parameter |

MBBS in India |

MBBS Abroad |

|

Loan Limit (Unsecured) |

Up to ₹50 lakhs |

Up to ₹75 lakhs |

|

Loan Limit (Secured) |

Up to ₹2 crores |

Up to ₹1.5 crores |

|

Expenses Covered |

Tuition, exam, library, lab fees, books, stationery, laptop, uniform, hostel/accommodation, insurance, travel |

Tuition, exam, library, lab fees, books, stationery, laptop, uniform, hostel/accommodation, insurance, travel |

|

Interest Rate |

Starts from 8.55%; higher for non-collateral loans |

Starts from 8.55%; higher for non-collateral loans |

|

Repayment Period |

12–15 years (including moratorium) |

12–15 years (including moratorium) |

|

Moratorium Period |

Course duration + 12 months |

Course duration + 12 months |

|

Co-Applicants |

Parents, sibling, spouse, parents-in-law |

Parents, sibling, spouse, parents-in-law |

|

Collateral Requirement |

Liquid collateral: 1.1× loan; Immovable: 1.25× loan |

Liquid collateral: 1.1× loan; Immovable: 1.25× loan |

|

Repayment During Moratorium |

Not specified |

Optional if university is on prime list; else simple interest to be paid |

Whether you’re pursuing medicine in India or overseas, explore all education loan options for MBBS students that cover tuition, living expenses, and more.

Now that you are reading about education loan for MBBS, we assume you are aware of the MBBS fees. If not, do have a look at this blog: MBBS Fees 2024: Private/Government College Fees Structures

People Also Ask

If your MBBS university is on a lender’s prime list, you may get an optional moratorium without paying interest. For non-prime universities, simple interest during study is usually required.

Propelld offers up to ₹30 lakhs without collateral, making it easier for students to fund MBBS in private or government colleges.

Education Loan for MBBS Interest Rates

Given below are the interest rates on education loans for different lenders:

|

Bank/NBFC |

Interest Rate |

|

13.70% p.a. onwards |

|

|

8.55% p.a. onwards |

|

|

9.25% p.a. onwards |

|

|

12.55% p.a. onwards |

|

|

9.50% p.a. onwards |

|

|

11.25%–16.50% p.a. |

|

|

11.75%–13.80% p.a. |

|

|

11.00%–16.00% p.a. |

|

|

11.25%–15.50% p.a. |

At Propelld, our interest rates start from as low as 11% for a profile with good academic records and salaried co- applicant. However, the interest rate might vary across profiles.

People Also Ask

Get your Loan Disbursed 10 times Faster than Banks. Apply Now.

For private MBBS colleges where fees is usually higher, NBFCs like Propelld are often better suited than banks because they finance higher ticket sizes without collateral.

Calculate Your EMI for MBBS Education Loan

Calculating your EMI (Equated Monthly Instalment) for an MBBS education loan is essential for effective financial planning. Propelld offers a dedicated and easy to use EMI calculator that helps you estimate your monthly payments based on your loan amount, interest rate, and repayment tenure.

- Just check out Propelld Education Loan EMI Calculator.

- Enter Your Loan Amount that you wish to borrow.

- Choose the duration (in years or months) over which you plan to repay the loan. Input the Interest Rate

Once all details are entered, the calculator will instantly display your estimated monthly EMI, total interest payable, and the overall repayment amount.

Eligibility Criteria for MBBS Education Loans

The basic eligibility criteria for MBBS education loans across most lenders are:

Understanding the education loan eligibility and application process is crucial for students to ensure a smooth approval experience, especially when applying for medical courses, and this knowledge becomes even more relevant while exploring education loans for MBBS students, as these often involve higher loan amounts and specific course-related requirements.

Documents Required for MBBS Education Loans in India

Securing an education loan for MBBS studies in India requires submitting a set of documents to ensure the loan process goes smoothly.

Essential documents that are primarily required are:

Address Proof: Bank account statement, Passport, Electricity bill, Aadhar Card, Voter ID, Telephone bill, Ration card.

Before you start your medical education journey, do have a look at the course structure for MBBS: MBBS Subjects For 2024: Year-Wise Syllabus And Structure.

How to Apply for an Education Loan for MBBS?

Most banks and financial institutions offer dedicated education loan schemes for MBBS aspirants, with both online and offline application options.

Below is a comparison table outlining the step-by-step process for applying online and offline, helping you choose the method that best suits your needs.

Online Process

- Visit the official website of the chosen bank or lender and navigate to the education loan section.

- Click “Apply Now” or the relevant link to start your application.

- Select the appropriate loan scheme for MBBS.

- Fill out the online application form with accurate personal, academic, and loan details.

- Upload scanned copies of all required documents.

- Submit the application online and track its status.

- Respond promptly to any additional requests from the bank.

- Await approval and disbursement updates from the lender.

Offline Process

- Visit your nearest branch of the chosen bank or lender.

- Request and collect the education loan application form.

- Fill out the form carefully with all required details.

- Attach physical copies of all necessary documents like admission letter, academic records, etc.

- Submit the completed application and documents at the branch.

- The bank will process and verify your documents.

- Attend any in-person verification or interviews if required.

- Follow up regularly with the branch for status updates.

- Receive approval and loan disbursement details from the lender.

Tips for a Successful Loan Application

Follow these simple yet effective steps to improve your chances of getting your education loan approved smoothly and quickly.

What to Avoid During the Application Process

Steer clear of these common mistakes that can delay your loan approval or negatively affect your eligibility.

Education Loan for MBBS: With & Without Collateral

Without Collateral

- Loan up to ₹40 lakh for tuition and living costs

- Interest rates from 9.55%

- Repayment up to 15 years (course + 6–12 months moratorium)

- Offered by: ICICI Bank, Axis Bank, IDFC, Propelld, InCred, Avanse, Auxilo, HDFC Credila

With Collateral

- Loan up to ₹2 crore against property or deposits

- Interest rates from 8.55%

- Flexible repayment up to 15 years

- Offered by: SBI, Bank of Baroda, ICICI, Axis, HDFC Credila, Avanse

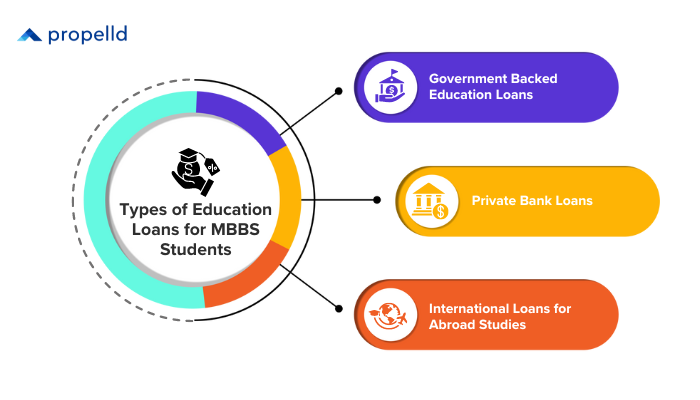

Types of Education Loans Available for MBBS Students

Government-Backed Loans

Government Backed Loans are offered by government agencies or banks in partnership with the government. For example, in India, the government offers the Central Sector Interest Subsidy Scheme (CSIS) for students from economically weaker sections, which covers the interest on the education loan during the moratorium period. These kinds of loans offer several advantages such as lower interest rates, flexible repayment options, and longer repayment tenures. This makes education loans more affordable for students pursuing MBBS.

Private Bank Loans

Private banks also offer education loans for MBBS students, with competitive interest rates and convenient repayment terms. Private bank loans may have faster processing times and more flexible eligibility criteria compared to government loans. Additionally, some private banks offer special schemes for medical students, including higher loan amounts and lower interest rates for top-ranking institutions.

International Loans for Students Studying Abroad

For MBBS students studying abroad, international education loans are a popular choice. These loans are offered by financial institutions or banks in the student's home country and cover the education expenses of a college situated abroad. Like other loans, these are also designed to cover the cost of tuition, living expenses, and other related costs. International loans often have competitive interest rates and flexible repayment options.

Do check out all details about Education Loan for Abroad Education in 2025 here.

Education Loan for Medical Students in India- Various States

Education loans for MBBS students in India are crucial financial tools that enable aspiring doctors to pursue medical education without being limited by financial constraints. Different states and banks offer a range of schemes tailored to the needs of medical students, with varying eligibility criteria, loan amounts, and benefits.

In Karnataka, Indian nationals with confirmed admission at a recognized institution can apply for education loans for MBBS, usually requiring a parent or guardian as co-applicant. Documentation includes admission proof, academic records, ID, address, and income proof.

In Maharashtra, students with secured MBBS admission can access schemes like the Model Education Loan and Maha Scholar Education Loan from Bank of Maharashtra. Co-applicants are required, collateral is not needed for loans up to ₹7.5 lakhs, and the average interest rate is generally around 10.1% per annum. Repayment is up to 15 years, with a moratorium of the course period plus up to a year. They can also get loan from regular private banks and NBFCs.

Delhi students can get loans up to ₹1 crore from banks, with a family co-applicant and collateral for higher amounts. The average interest rate for education loans in Delhi is typically about 10.2% per annum. Required documents are academic records, admission proof, ID, address, and income proof. Repayment is flexible, including a moratorium for the course and up to 12 months.

For MBBS in Tamil Nadu, loans cover all major expenses, with co-applicants and collateral needed for larger amounts. Interest rates from nationalized banks are typically between 8.85% and 11.60% per annum. Repayment terms are up to 15 years with a moratorium for the course plus 6-12 months, and documentation requirements are similar to other states.

Schemes for MBBS Education Loan

Several leading banks and financial institutions in India offer specialized loan schemes for MBBS students. Below is an overview of prominent MBBS education loan schemes available to aspiring medical professionals.

Scholarships and Grants for MBBS

For students exploring alternatives to MBBS education loans, scholarships and grants can significantly reduce financial pressure. These are offered by government bodies, universities, and private organizations, based on merit, need, or category.

Top MBBS Scholarships in India

- National Scholarship Portal (NSP): Includes Central Sector and Top-Class Education Schemes for SC/ST students.

- Dr. Abdul Kalam Scholarship: Supports meritorious students from economically weaker sections.

- AICTE Pragati Scholarship for Girls: Encourages female students to pursue medical education.

- Maulana Azad Scholarship: For minority students pursuing professional degrees like MBBS.

- State Scholarships: Merit- and need-based schemes by states like Punjab, Haryana, and UP.

MBBS Scholarships Abroad

- Commonwealth & Rhodes Scholarships: Cover tuition and living costs in the UK.

- Fulbright Program: Offers full or partial funding for MBBS-equivalent courses in the USA.

- Erasmus Mundus: Funded by the EU for medical studies in Europe.

If scholarships don’t fully cover your expenses, or if you arent eligible for one, explore Propelld’s Education Loan for MBBS- designed for both domestic and abroad students with flexible, no-collateral options.

Rejected by Banks for Education Loan? Don't Worry, Propelld has Got Your Back. Check Your Eligibility Now!

Securing an education loan for your MBBS studies can be challenging, given the high competition and limited seats in medical colleges. But it's the most important step in your path of “how to become a doctor.”

Propelld understands these challenges and offers a seamless solution tailored to your needs.

While most banks take 2-3 weeks to sanction your loan, Propelld does it in 24-48 hours.

Choose Propelld for a hassle-free education loan experience and pave the way for your successful career in medicine!