.svg)

Managing your education loan can be stressful, especially when the terms offered by your current lender aren't as favourable as they once seemed. The good news? You're not stuck.

Education loan transfer, also known as education loan takeover, allows you to shift your existing loan from one bank to another, often getting better interest rates or more flexible repayment options.

In this blog, we'll walk you through everything you need to know about transferring your loan and how it works.

What is an Education Loan Transfer?

Education loan transfer simply moves your existing loan from one bank to another. It's typically done when the new bank offers lower interest rates, better loan terms, or more flexibility, making it easier for you to repay the loan. The bank taking over your loan pays off your old lender, and you begin repaying the new bank under the revised terms.

Can We Transfer Loan from One Bank to Another?

Absolutely! Transferring your loan from one bank to another is possible, and many students and parents do so to secure better deals. Most banks in India and globally offer this service as part of their lending products, with the Reserve Bank of India (RBI) setting clear guidelines that govern this process.

If you're planning to switch your lender, understanding the complete education loan balance transfer process is essential to make a cost-effective and seamless transition.

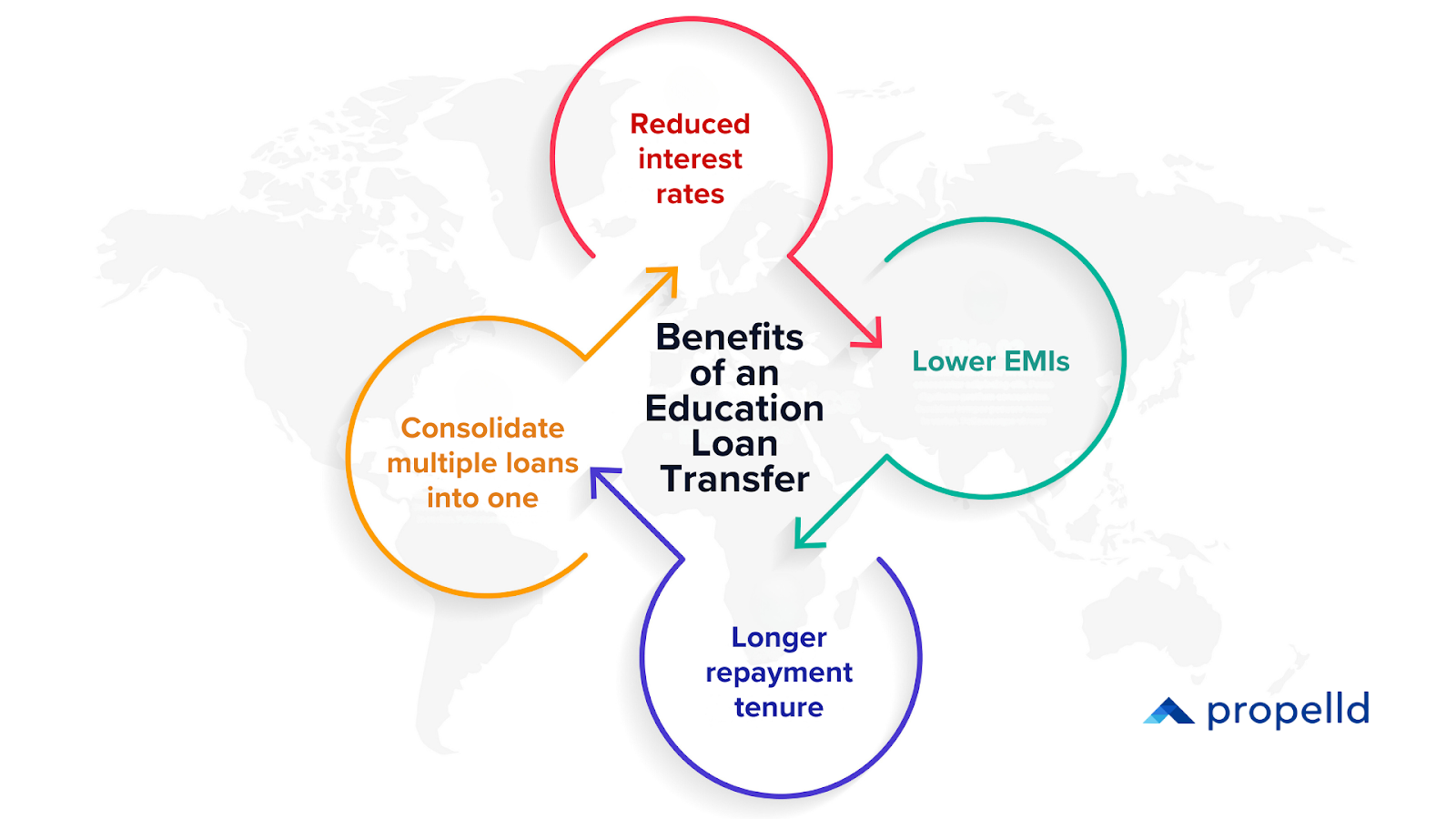

Key Benefits of an Education Loan Transfer

- Reduced interest rates

- Lower EMIs (Equated Monthly Instalments)

- Longer repayment tenure

- Option to consolidate multiple loans into one

Also Read: Education Loan by the Government: Eligibility and Application 2026.

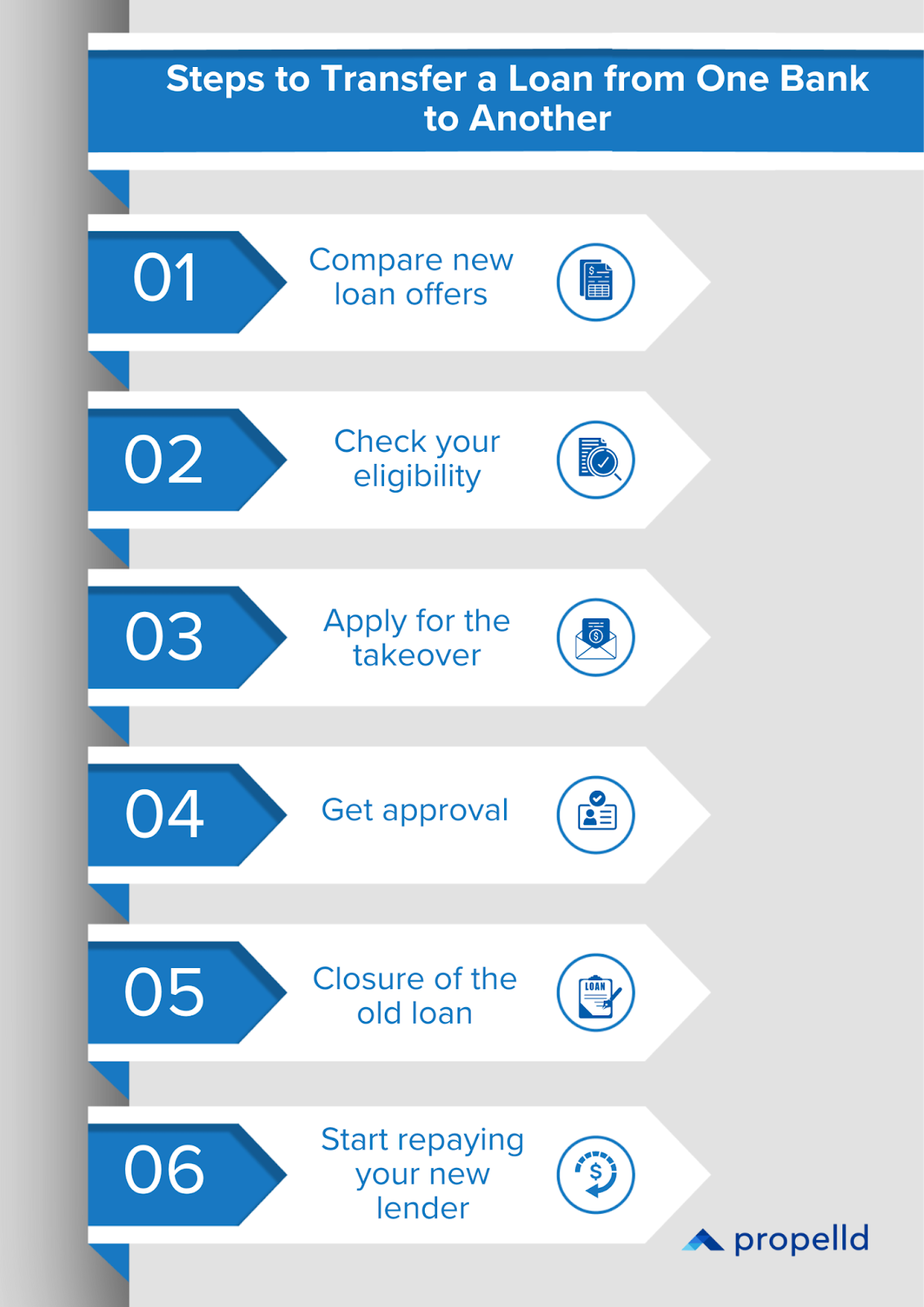

How to Transfer a Loan from One Bank to Another?

Transferring an education loan involves several steps, but it's not as complicated as it might sound. Here's a simple step-by-step guide:

1. Compare new loan offers

Research multiple banks and compare their interest rates, processing fees, and repayment terms.

2. Check your eligibility

Each bank has its eligibility criteria, typically based on your repayment history, credit score, and financial background.

3. Apply for the takeover.

Submit a loan transfer application and the necessary documents to the new bank.

4. Get approval

Once approved, the new bank will issue a sanction letter stating the new loan terms.

5. Closure of the old loan

The new bank disburses the loan amount directly to your current bank to close the existing loan.

6. Start repaying your new lender

You now repay the new lender as per the revised EMI schedule.

Suggest Read: Education Loan Scheme by Narendra Modi: List of Banks 2026

Get upto 100% Education Fees Financed with Propelld. Simplified Processing Dedicated Support.

Eligibility Criteria for Education Loan Transfer

Before transferring your loan, you need to meet some eligibility requirements. Here's what banks typically look for.

| Eligibility Criteria | Description | Importance |

|---|---|---|

| Good Repayment History | A consistent track record of paying your EMIs on time with no defaults or delays in your previous payments. | Ensures the borrower is financially responsible and capable of handling debt. |

| Credit Score | Reflects your creditworthiness based on previous loans and financial activity. Banks usually require a score of 650 or above for loan transfers. | A high score (ideally 750+) improves your chances of getting a better deal on interest rates and repayment terms. |

| Income Details of Co-Signer | The cosigner's income and financial status are critical if the borrower has no income. If needed, the bank will assess the cosigner's ability to take responsibility for the loan. | Ensures that there is financial backing in case the borrower (student) cannot make timely payments. |

| Co-Signer's Credit Score | The co-signer's credit score must also be high (700+), especially if the borrower doesn't have a credit history or income yet. | An excellent co-signer credit score strengthens the loan application and increases the likelihood of approval for transfer at competitive interest rates. |

| Collateral Documents | If the loan is secured, the new bank will require collateral-related documents, such as property or asset valuations, and the new lender will re-assess the collateral. | The new bank will reevaluate the collateral's value to ensure it adequately covers the loan, especially for more significant amounts. |

| Transfer of Lien | If the property is used as collateral, the lien (legal claim on the property) must be transferred from the original lender to the new one. | Ensures the new lender has a legal claim on the collateral if the borrower defaults, protecting the bank's interest. |

| Fresh Valuation by New Bank | The new bank may request a fresh collateral valuation to ensure it retains sufficient value over time. | Re-assessing the value of collateral ensures that the bank's risk is minimal in case of default, especially for secured loans. |

Also Read: Jansamarth Education Loan: Eligibility, Documents and How to Apply.

Documents Required for Education Loan Transfer

When transferring your education loan, the bank will request documents to complete the process.

| Document | Description | Purpose |

|---|---|---|

| Loan Sanction Letter | Your current bank issued an official letter stating that your loan was approved. It includes the loan amount, interest rate, and repayment terms. | Confirm the loan's original terms and prove its existence to the new lender. |

| Repayment Track Record | A record showing at least six months of consistent EMI payments to your current bank. | Verifies repayment discipline and financial responsibility, helping the new bank assess your creditworthiness. |

| Identity Proof of Borrower & Co-Signer | The borrower and co-signer must present an Aadhar card, PAN card, passport, or other government-approved ID document. | Establish your and your co-signer's identity for verification purposes. |

| Income Proof of Borrower & Co-Signer | Salary slips, bank statements, or income tax returns for both borrower and co-signer. | It helps the new bank evaluate your repayment ability and the co-signer's financial backing in case of default. |

| Collateral Documents (If Secured Loan) | Legal documents related to the collateral, such as property deeds or fixed deposit certificates. | The new bank needs to verify the value and legality of the collateral to ensure it adequately covers the loan in case of default. |

| Admission and Course Details | The official admission letter and course details from the educational institution, including the course duration and total fees, are attached. | Confirms that the loan is being used for educational purposes and assists in calculating the loan tenure based on the course duration. |

To successfully transfer your education loan, you'll need to arrange key documents required for education loan such as the original sanction letter, repayment history, and collateral papers.

Get your Loan Disbursed 10 times Faster than Banks. Apply Now.

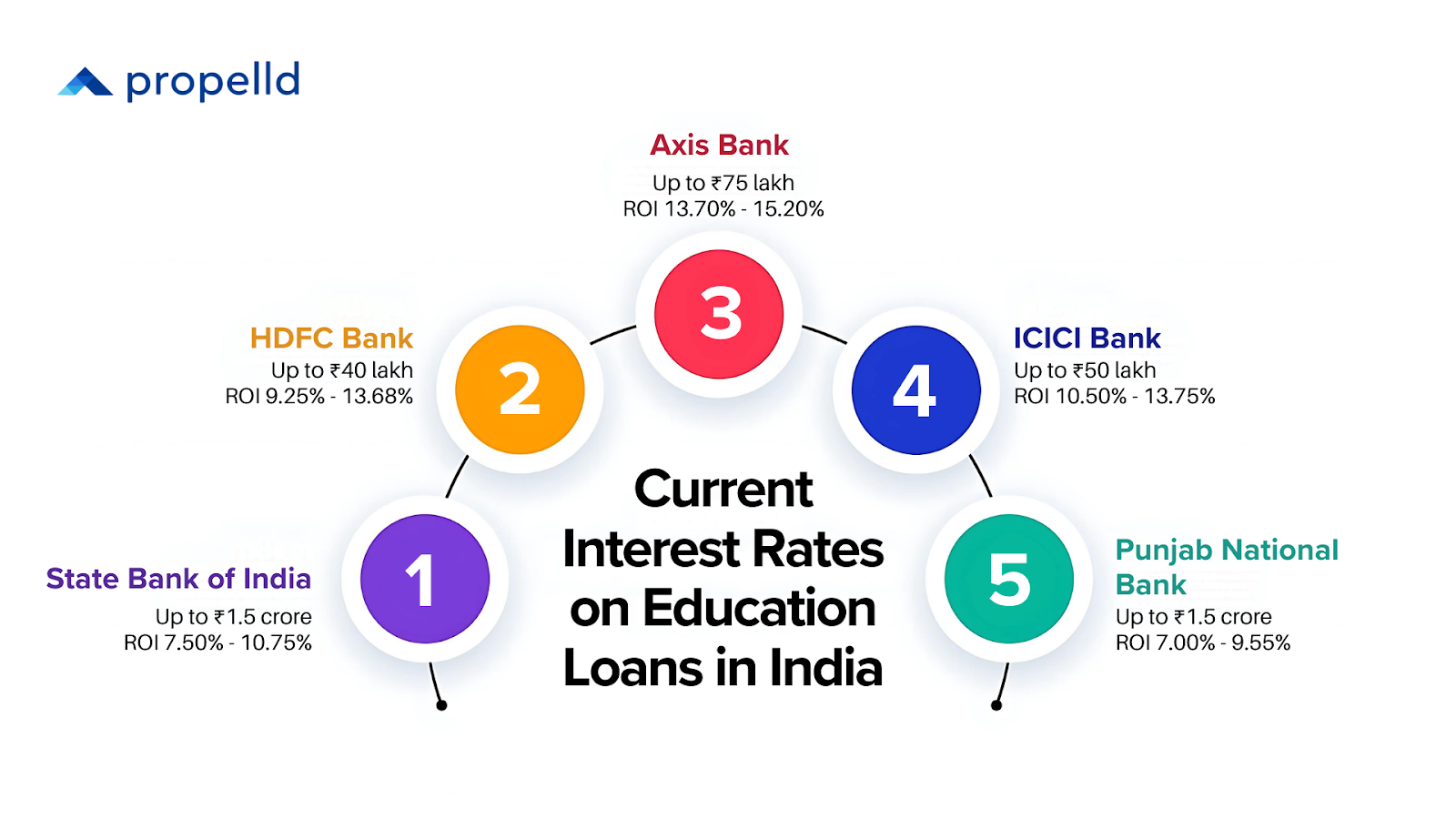

Current Interest Rates on Education Loans in India

Banks in India offer various interest rates on education loans. The figures below are indicative as of 2025-26 and are subject to change; always verify current rates directly with your lender before making a decision.

| Bank Name | Interest Rate (p.a.) | Loan Amount | Repayment Tenure |

|---|---|---|---|

| State Bank of India | 7.50% - 10.75% | Up to ₹1.5 crore | Up to 15 years |

| HDFC Bank | 9.25% - 13.68% | Up to ₹40 lakh | Up to 15 years |

| Axis Bank | 13.70% - 15.20% | Up to ₹75 lakh | Up to 20 years |

| ICICI Bank | 10.50% - 13.75% | Up to ₹50 lakh | Up to 10 years |

| Punjab National Bank | 7.00% - 9.55% | Up to ₹1.5 crore | Up to 15 years |

The interest rate you receive will depend on several factors, including your credit score, loan amount, and repayment tenure.

To stay ahead of fluctuating rates, it's important to know how to get the best education loan interest rates by comparing lenders and understanding what influences rate changes.

How to Get a Lower Interest Rate During Education Loan Transfer?

When you're considering an education loan transfer, here are a few tips to help you secure a better deal:

1. Negotiate with your current bank first

Before transferring, try negotiating a better rate with your existing bank. They may offer a lower rate if they know you're considering leaving.

2. Check your credit score

A higher credit score (750 and above) can help you get lower interest rates.

3. Look for a particular scheme

Some banks offer reduced rates for specific courses or institutions.

4. Consider government schemes

The Central Sector Interest Subsidy Scheme (CSIS) offers interest subsidies on loans for economically weaker students in India.

When Should You Consider Transferring an Education Loan?

You should think about transferring your education loan if:

- Your current bank charges a high interest rate, and you've found better rates elsewhere.

- Your EMI payments are too high, and you'd like to extend your repayment tenure to reduce the monthly burden.

- You want to consolidate multiple education loans from different banks into one.

- Your current bank's customer service or flexibility isn't meeting your needs.

Is Education Loan Transfer Right for You?

Transferring your education loan is an excellent option if you:

- Are struggling with high interest rates.

- Need more flexibility in terms of EMI or loan tenure.

- Want to consolidate multiple loans into one.

However, it's essential to weigh the processing fees, penalties, and other charges before switching. Always compare multiple offers and ensure that the new terms are genuinely better.

Difference Between Education Loan Transfer and Education Loan Takeover

Though often used interchangeably, there's a subtle difference between education loan transfer and education loan takeover:

| Criteria | Education Loan Transfer | Education Loan Takeover |

|---|---|---|

| Primary Objective | To secure better interest rates or EMI without changing the core loan structure. | Change the loan terms, such as repayment period, interest rate, and loan amount. |

| Loan Structure | It remains the same (same loan amount and tenure). | Can be modified (tenure, interest rate, loan amount). |

| Top-Up Facility | Generally not available. | Often includes the option for additional funds or top-up loans. |

| Collateral Transfer | Required if the original loan is secured. | Additional documents may be needed if the original loan is secured. |

| Loan Consolidation | Rarely used for consolidation of multiple loans. | Often used for consolidating multiple education loans. |

| Documentation | Essential documentation (e.g., loan sanction letter, ID proof). | It requires more documentation, including a re-evaluation of loan eligibility. |

| Flexibility | There is less flexibility in terms of altering the loan structure. | High flexibility to modify loan terms. |

| Approval Process | Generally faster and less complex. | It is more complex, involving re-evaluation and new financial checks. |

| Best For | Borrowers who want a lower interest rate without changing much of the loan's structure. | Borrowers who need more comprehensive changes, including loan restructuring or top-ups. |

| Repayment Tenure Extension | Possible but limited. | Typically, it allows a more flexible extension of the repayment period. |

| Interest Rate Adjustments | Focuses on lowering interest rates. | It may include significant adjustments to both interest rates and loan tenure. |

Get an Education Loan for Any College in India. 100% Fees Financed- Propelld Education Loan.

What Students Are Discussing About Transferring an Education Loan

Social media platforms like Quora provide a window into common student concerns about education loan transfers and repayment challenges.

A Quora user in Financially Fresh

Answered by Jeyakumar G, Nov 27, 2023

Question: "Can we transfer my education loan to another bank if my EMI has started already? What is the procedure?"

Answer: "If it is a clean loan (no property mortgaged), no bank will take over. In India, there are no rules for transferring unsecured education loans between banks. However, if it is a secured education loan (property mortgaged), there is a possibility. You can approach another bank and request a mortgage loan (loan against property). If the new bank is satisfied with your records, they may take over the education loan from the first bank, and your EMI will continue with the new bank under a mortgage loan arrangement."

Insights

- Unsecured education loans cannot be transferred once EMIs start.

- Secured loans with property collateral may be transferred, usually converted into a loan against property.

- The new bank's approval depends on your financial history and documentation.

Pro Tip

If EMIs are a burden, first try to negotiate with your existing bank for lower interest or longer tenure. If you have collateral, compare offers from multiple banks before opting for a transfer.

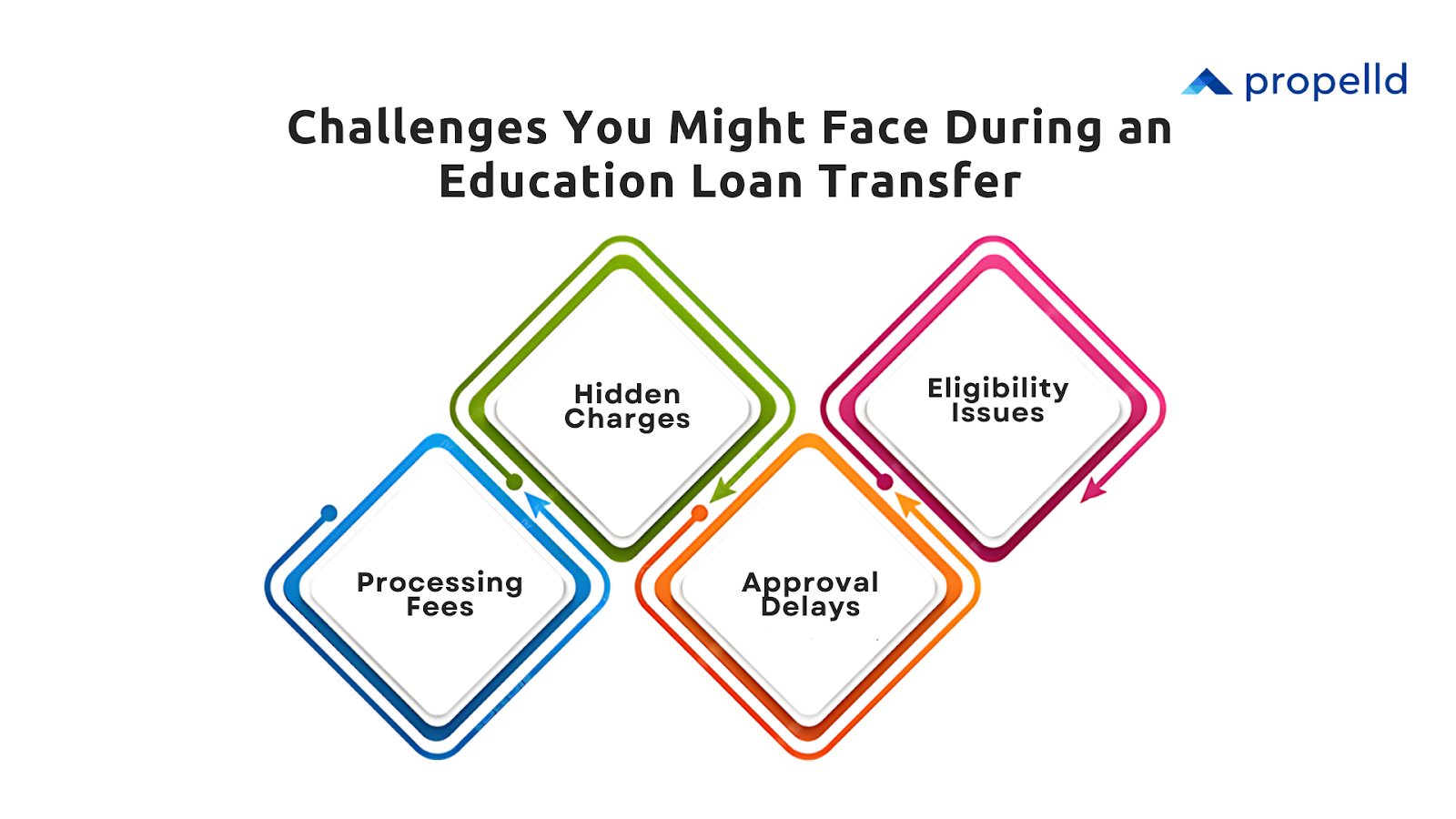

Challenges You Might Face During an Education Loan Transfer

Although transferring your loan sounds appealing, it's not without its challenges:

1. Processing fees

Some banks charge processing fees (typically 0.5% to 1% of the loan amount, as of 2025-26; varies by lender and is subject to change) for the transfer.

2. Hidden charges

Check for hidden costs like foreclosure penalties or prepayment fees that could affect your savings.

3. Approval delays

The transfer process can take time, and delays might result in missed EMIs or penalties.

4. Eligibility issues

Poor credit history or insufficient documentation could result in your application being rejected.

An education loan transfer can provide significant financial relief, especially if you're paying a high interest rate or struggling with EMIs. By understanding the process, researching banks, and comparing terms, you can take control of your loan and reduce your financial burden.

Propelld offers student-specific education loans, which you can choose according to an assessment of direct or indirect liabilities in education loans.